DILLARD'S (DDS)·Q4 2026 Earnings Summary

Dillard's Q4 2026: EPS Beats Big, But Revenue Miss and Flat Comps Sink Stock 8%

February 24, 2026 · by Fintool AI Agent

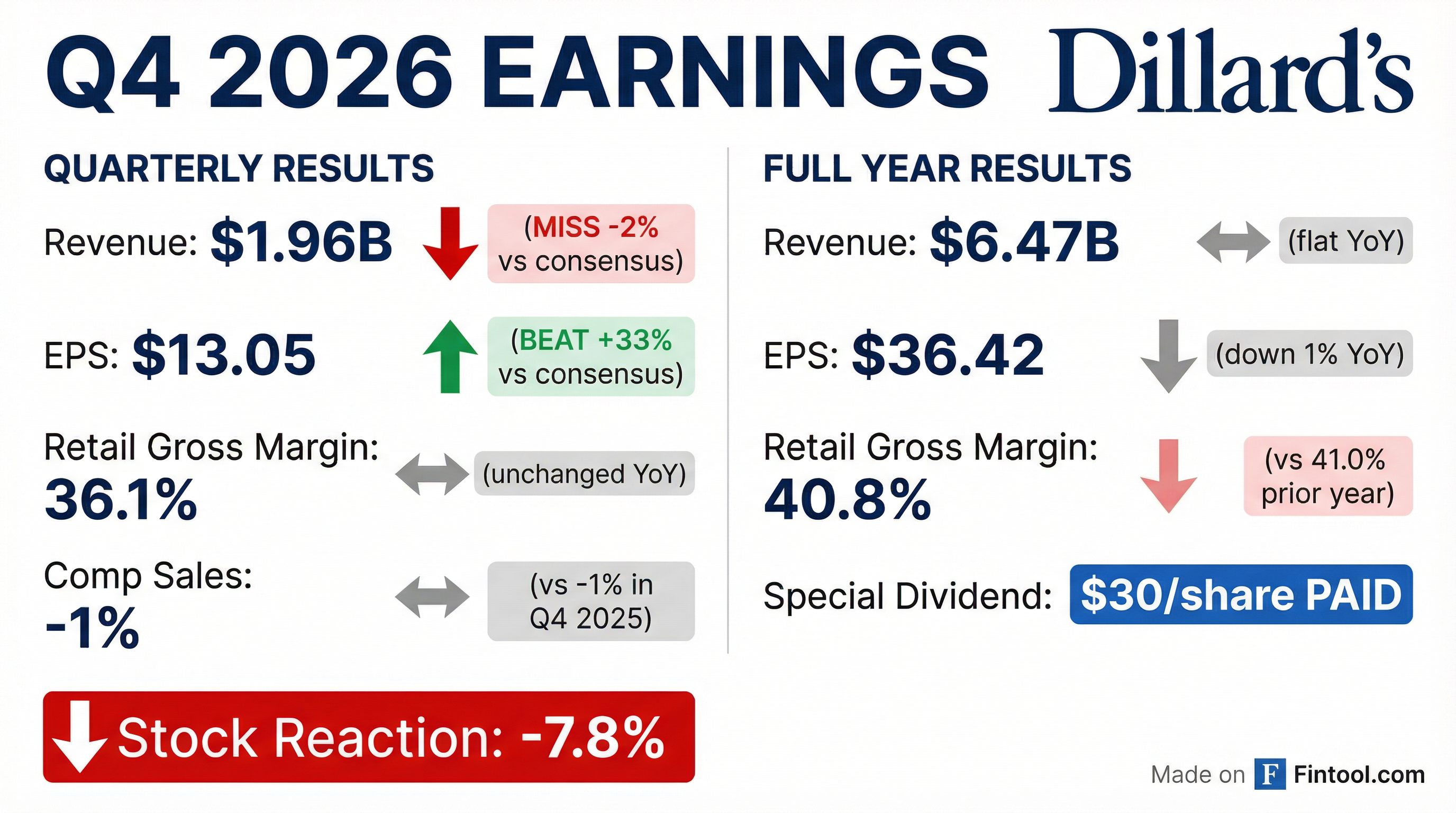

Dillard's delivered a tale of two metrics in Q4 2026: earnings per share crushed expectations by 33%, but revenue came up short and comparable store sales declined 1%. The market focused on the top-line weakness, sending shares down nearly 8% on the day.

CEO William T. Dillard, II called it "a respectable year" while highlighting the company's 40.8% retail gross margin achievement and record $30 per share special dividend.

Did Dillard's Beat Earnings in Q4 2026?

Mixed. EPS crushed estimates; revenue missed.

*Normalized EPS excludes one-time items including $0.73/share gain from property sale and $2.24/share tax benefit from ESOP dividend deduction. Values retrieved from S&P Global.

The EPS beat was substantial, but investors appear concerned about the top-line miss and ongoing traffic challenges in department stores.

Full Year Summary

What Drove the Quarter?

Comparable Store Sales

Comp sales declined 1% in Q4, with management noting that over a third of stores were disrupted by a winter storm during the third weekend of January.

Category performance (Q4 vs prior year):

For the full year, total retail sales and comp sales were unchanged — a notable achievement in a challenging retail environment.

Margin Analysis

Retail gross margin held flat at 36.1% in Q4 despite the promotional retail environment.

- Ladies' apparel and juniors'/children's margins improved moderately

- Men's apparel & accessories margins declined moderately

- All other categories held steady

Operating expenses rose to 23.6% of sales (vs 22.4% last year), driven primarily by payroll and payroll-related expenses.

How Did the Stock React?

Dillard's shares dropped 7.8% on the earnings release, closing at $595.88 after opening at $608.57.

The selloff reflects investor concern about:

- Revenue miss — top-line growth remains elusive

- Negative comp sales — traffic challenges persist

- Rising SG&A — labor costs pressuring margins

- No guidance raise — company provided flat-to-modest expectations for FY 2027

What Did Management Guide?

Dillard's provided the following estimates for FY 2027:

The 40% increase in planned capex ($130M vs $93M actual) stands out. The company is opening a new 160,000 square foot store at The Mall at Fairfield Commons in Beavercreek, Ohio in March 2026.

Consensus Expectations for FY 2027

*Values retrieved from S&P Global.

Analysts expect EPS to decline 21% next year, suggesting the market anticipates margin normalization and continued topline pressure.

Capital Allocation Highlights

Dillard's continues to prioritize shareholder returns:

Dividends:

- Paid a $30 per share special dividend in FY 2026 — the largest in company history

- Prior year: $25 per share special dividend

- Total cash dividends paid: $484.8M

Share Repurchases:

- Repurchased ~300,000 shares for $107.8M at an average price of $359.16

- $165.2M remaining under the May 2023 authorization

- Shares outstanding: 15.6M (vs 15.9M a year ago)

Balance Sheet Strength:

- Cash & equivalents: $861.5M (vs $717.9M)

- Short-term investments: $211.5M

- Total liquidity: ~$1.1 billion

- Total debt: $321.7M (current + long-term)

- Stockholders' equity: $1.78B

What Changed From Last Quarter?

*Q3 typically has higher margins; Q4 is the holiday quarter with more promotional activity.

Q4 is seasonally the largest quarter for department stores. The sequential increase is expected, but year-over-year comparisons show pressure.

Historical EPS Performance

*Values retrieved from S&P Global.

Dillard's has beaten EPS estimates for 5 consecutive quarters, but the stock's reaction today suggests the EPS beat alone isn't enough when revenue and traffic disappoint.

Key Risks and Concerns

- Traffic headwinds — Comp sales flat-to-negative despite strong merchandising

- Rising labor costs — SG&A up 60 bps YoY as a percentage of sales

- Inventory build — Inventory up 2% despite flat sales

- Department store secular decline — Mall traffic continues to erode

- Tariff uncertainty — Management cited trade disputes and tariff impacts as risk factors

Store Footprint

Dillard's operates 271 stores (including 28 clearance centers) across 30 states, totaling 46.0 million square feet.

Upcoming opening: New 160,000 sq ft store at The Mall at Fairfield Commons in Beavercreek, Ohio (March 2026)

Forward Catalysts

- New store opening — Ohio location in March 2026

- Q1 2027 earnings — Watch for early spring selling trends

- Capital allocation decisions — Will they continue special dividends?

- Tariff policy clarity — Potential cost headwinds from trade policy

Bottom Line

Dillard's Q4 2026 illustrates the department store paradox: strong margin management and capital returns can't fully offset persistent top-line challenges. The company beat EPS by 33% and returned nearly $600M to shareholders through dividends and buybacks, but flat comps and a revenue miss dominated the narrative.

With $1.1 billion in liquidity, a clean balance sheet, and disciplined operations, Dillard's remains well-positioned to weather the secular headwinds facing traditional department stores. But until traffic trends improve, the stock may continue to face skepticism from growth-focused investors.

Report generated by Fintool AI Agent on February 24, 2026. Data sourced from company filings and S&P Global.